There’s been a lot of talk about the demise of department stores and malls In general. So when I heard about the $5.8 billion buyout bid for Macy’s, an American department store chain, I found myself intrigued.

By the way, the offer to take the company private was a 20.76% premium to Macy’s previous trading day closing price.

So let’s do a Roulette post and take a peek at the company’s financials. Let’s see what we can discover in two minutes.

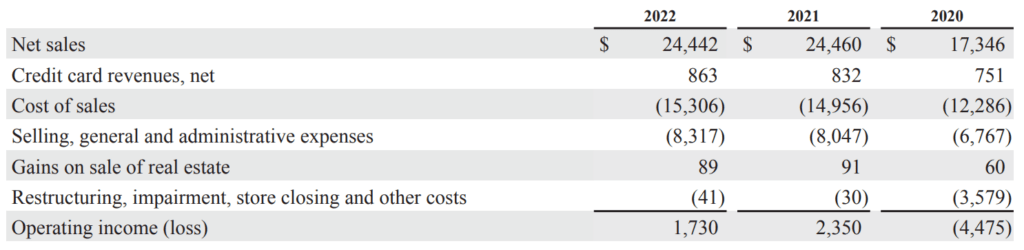

Income Statement: Random Observations

First of all, I want to highlight the top of the income statement from Macy’s 2022 Annual Report.

The Covid year adds a nice contrast. We can see several interesting things here.

- Compared to 2021, net sales in 2020 were 29.08% less.

- Credit card revenues rose only 11.08% from 2020 to 2021. As expected, credit card spending remained significant during the pandemic (lower amounts of spending and higher credit card use).

- Net sales were similar in 2022 and 2021. However, both the cost of sales and SG&A were higher in 2022.

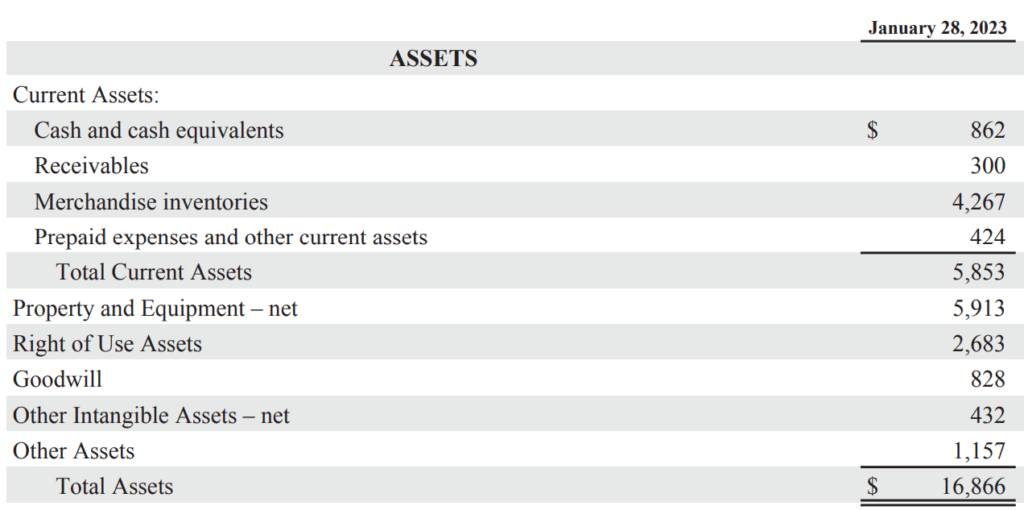

Balance Sheet: What Everyone’s Talking About

Macy’s real estate portfolio was highlighted as a major reason for the investors’ interest. Just looking at real estate alone, JP Morgan’s analysts say that Macy’s portfolio is worth $8.5 billion.

What jumps out here is the value of P&E, which is valued higher than Macy’s total current assets.

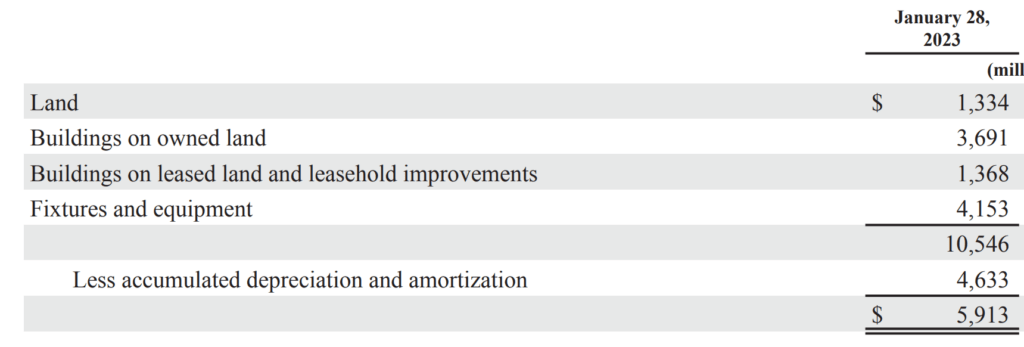

If we go in even deeper, we can break the numbers down further. Here is the section highlighting the major classes of Property and Equipment.

The second line is pretty significant. Though apparently Macy’s Herald Square property is worth around $3 billion alone.

If you want to keep reading, take a look at SC’s previous business post about reasons companies/teams/arenas rebrand.